On October 22, Jack Dorsey, CEO of Twitter and Square tweeted the now infamous…

That tweet was met with wide ridicule, with many responding that he is wrong, and that the definition of hyperinflation is actually 50% increase in prices per month.

That of course is not happening.

However, is he seeing something in the distant future that we aren’t? After all, as CEO of Square he is seeing real time data and trends in a vast array of financial transactions.

Whether it’s hyperbole or not, I’m pretty sure many agree that inflation is out of control, and not as “transitory” as the various central banks suggest.

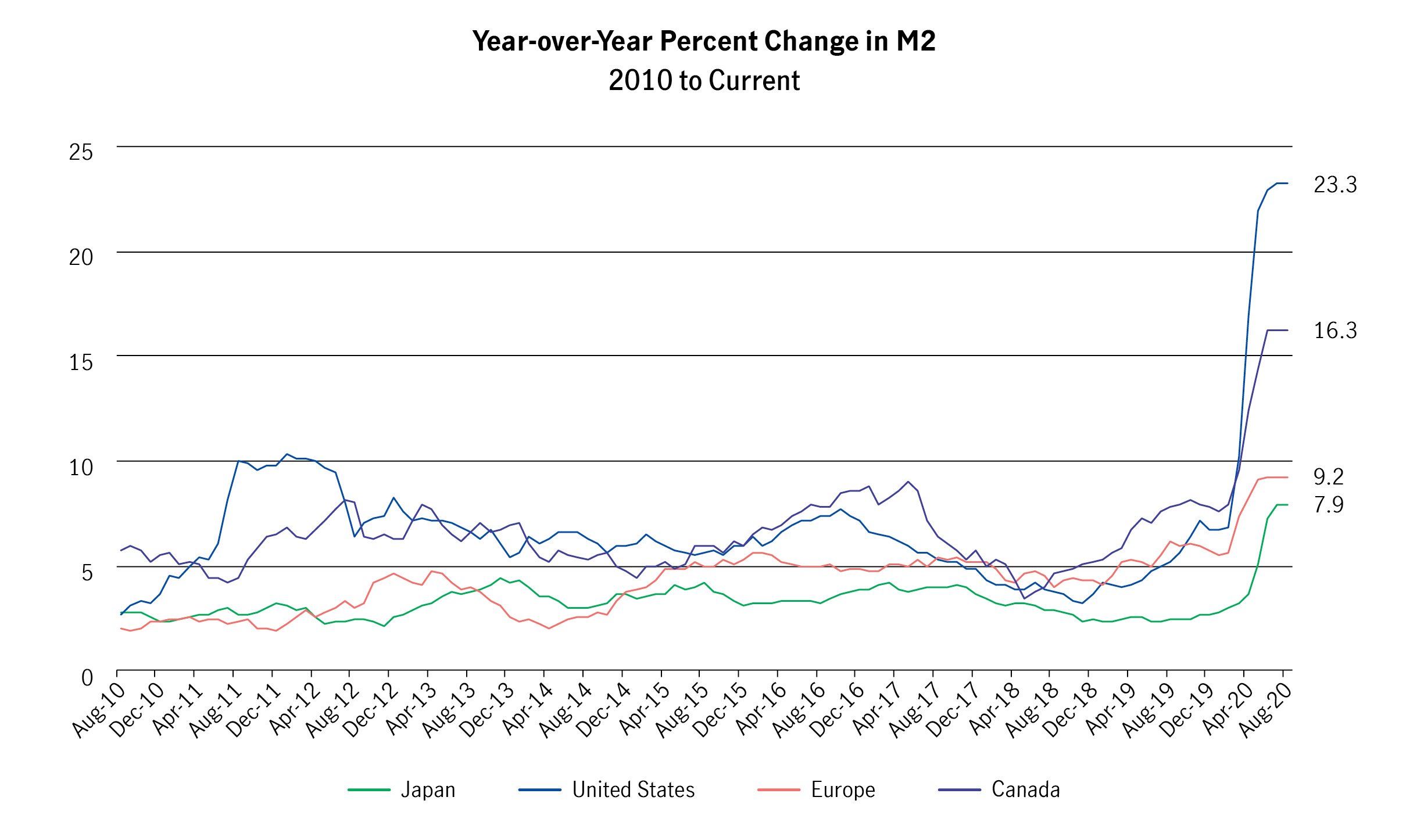

In Canada, the annual inflation rate rose to 4.7% in October, the highest in almost 20 years. Without the hedonic adjustments (i.e. techniques used to show a lower inflation rate based on product improvements), many argue that actual inflation is closer to 10 to 15%.

We don’t really need charts and data to tell us that inflation is running red hot. All of us now feel the very real increase in prices everywhere, from shelter to fuel, and food to labour.

The narrative around this inflation is that supply chain issues, easy credit, and the reopening of the economy has led to steep price increases.

But if you peel back the onion, you’ll know that we are actually towards the tail end of a long term debt cycle. And I’m not kidding when I say long.

As in 80-90 years long.

This is where governments around the world (led by the US) become massively indebted, and the only way to pay that debt is to borrow more money (by issuing bonds and having them purchased in the open market or by freshly printed money by central banks).

So what the heck does this have to do with real estate?

Stick with me here. I feel that we NEED to understand this before we can make education decisions about our real estate portfolios.

I am not an economist, but I try my best to understand these things with an unbiased view for my own sake, as I have to navigate the same waters as everyone else to protect myself as much as possible.

Really this analysis is for selfish reasons, but I’d like to share it to see if it might help you. I certainly may be entirely wrong, but I do believe it, and my actions are congruent with these thoughts.

You can agree or disagree, or take parts of it that may be helpful for you. Or dismiss it altogether if you don’t agree with it. These are just my honest thoughts.

And of course, none of this is investment advice.

The Money Printers Going BRRRRRR

All of this money printing (fancily called “quantitative easing”) forces interest rates down (where we have been for over a decade).

And with all that essentially “free” money, people are able to borrow at almost no cost, and place them in assets (stocks, real estate, commodities and other tangible assets).

This really is the reason why we’re seeing the level of inflation where it is. The story of supply chain issues is secondary.

Effect On Real Estate

So how does this affect our real estate?

Because inflation is now part of the mainstream narrative, it appears the various central banks (led by the US) are forced to raise interest rates.

Or are they?

In Canada, it is suggested that there will be 8 interest rate hikes in the next couple of years.

This type of narrative from the government is called “forward guidance”, which is meant to help tame inflation, without actually crashing the economy and having to increase payments on their actual debts and liabilities.

Whether they will actually raise rates is another question

Our government (and most governments around the world) are caught between a rock and a hard place.

On the one hand, inflation is out of control. In order to tame inflation, they need to raise interest rates.

On the other hand, if they raise interest rates, they will risk crashing an already fragile economy. Or even worse, crashing themselves.

You see, most state governments are in a massive amount of debt. Any large interest rate hikes are going to significantly increase the amount of money they have to pay back, just in interest alone.

And Canada is just a tiny piece of the pie. We’re really just following along with the big guys (US and Europe).

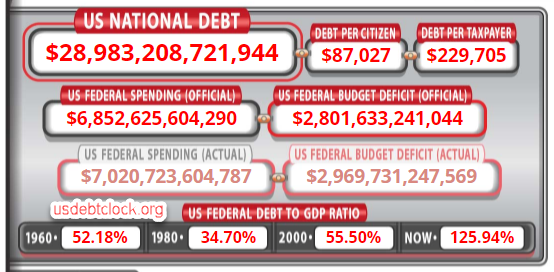

To understand this better, it helps to look at the US. Look at the debt burdens in the US.

Looking at these numbers, the question is not when will things get back to normal, but rather

- When will it end? And

- What will the end look like?

Unfortunately, no one has the answer to these two questions.

But we do know for sure that this debt will NEVER be paid back, and there’s really no going back to “normal” until a new system emerges. It’s just math.

This is not like the inflation of the late 1970s where they were able to then reign it in with double digit interest rates. Sure, they crashed the economy temporarily, but the government remained solvent because debt burdens weren’t as high back then.

If you do the same thing this time, you will crash both the economy, and the government themselves.

On Oct 29, 1981, the interest rates were around 20%. The debt burden at the time was $75 billion in Canada, meaning annual interest payments required from the government was around $15 billion. A great time to be a saver.

Forty years later on Oct 29, 2021, the interest rate is at 0.25%, but the debt has increased over 15x to $1.17 trillion. Assuming rates go up to 4%, the annual interest payments alone by the Canadian government would be over $45 billion annually.

This doesn’t even include all the provincial and municipal debts and liabilities that are only currently solvent because of near zero rates.

If rates go to 4%, don’t expect potholes to get repaired.

My guess is that they will try to raise rates slightly in the next year, probably a paltry 0.25% or 0.5% so that they can say, “See, we’re actively doing our job to tame inflation by raising interest rates”. This will likely have little effect, and they will probably allow inflation to run hot.

Keep in mind that this interest rate is not the same as the borrowing rate at your lender. It’s the overnight lending rate between the central bank and the commercial banks.

Your borrowing rate will be a couple of percentage points higher depending on what the banks’ profit margin requirements are. But it will roughly move in tandem.

Okay enough about this macroeconomic gibberish. You want to know how this is going to affect your real estate.

No one has a crystal ball, but if it does end up going 1 to 2 percentage points higher in the next couple of years (which I don’t think it will), I doubt that would make a huge difference. And even going up 1 to 2 percent is a huge leap.

Some economists are saying they are going up to 4 to 5 percent. The only scenario where I see that happening is if inflation on the Consumer Price Index (CPI) is at 10% or higher (in which case real inflation might be something crazy like 20 to 25% – as we see from the hedonic adjustments).

If that happens, our government would have to figure out how to pay all these extra billions in interest payments on their debt. Of course that would likely mean that the central bank would need to print even more money to lend back to the Canadian government to pay their debts.

They do this by purchasing more Canadian bonds, putting the government and taxpayers into even more debt. This then turns into an uncontrollable spiral downward.

If this is confusing, think of it using this analogy.

You are unable to pay your credit card bill, and your credit card company issues you more credit in order to make minimum payments. This is kind of insane, but it’s how our system is being run right now.

What all this means is that inflation will likely continue to run red hot.

And what will that do to your real estate? Again, hard to say, but if inflation is a long term trend, then I simply cannot see how real estate can reverse in pricing, given all this credit that HAS to be issued to keep the game going.

I remember 10 years ago when building a legal basement suite cost around $40,000 all in, when it now runs around $120,000.

It helps to not think of the value of your house going up, but rather the purchasing power of your money going down. But if your debt is denominated in devaluing dollars, and your rates remain low, then you are effectively paying back with cheaper money.

The accounting system in our economy is broken, and is causing all of these weird market reactions, like 30% year over year price increases in housing.

This is not normal, and we truly are in the acceleration phase of a long term debt cycle.

Although the pandemic, immigration and constrained supply all have a role to play in accelerating housing inflation, these factors don’t play as big a role as the amount of credit that has been issued in the past 2 years, and even before the pandemic.

Some may argue that there is a way to get things back on track. We simply need to grow our way out of debt. This is still something our politicians still talk about as if it’s really going to happen at a large enough scale to dial down our debts.

Jeff Booth, author of The Price of Tomorrow, explains in his book that technological improvements have a huge deflationary effect, but our economic system requires inflation to keep going.

He cites that in the past 20 years, there has been roughly 200 trillion dollars pumped into the world economy in the form of credit, with only around 50 trillion of growth.

If you owned a business, and it cost you $20 to make $5 in revenue, how long would you keep that business running?

Now, given the extreme price increases in real estate in the past couple of years, it wouldn’t surprise me if the market remains flat or even has a pull back should there be a slight uptick in interest rates. This would probably be a good thing.

But given everything that we have outlined above, this train only seems to be going one direction as long as we are still living in our current long term economic debt cycle.

This cycle could end next year or in ten years. No one knows.

So What Should I Do?

I can’t tell you what you should do, but here’s what I am doing.

I myself will continue to push along on figuring out ways to add value to various properties, while adding the much needed housing units in our communities, and encourage those around me to do the same.

We cannot rely on the market itself, but rather look at it as the cherry on top if the market continues to go up.

Here’s what I will continue to work on.

This of course is not investment advice. Everyone’s situation is unique, and you need to figure out what makes sense for you given your unique circumstances and your risk tolerance.

I will continue to look for good buying opportunities where the strategies as part of my forced value ladder can be applied:

- Cosmetic improvements

- New second suite

- New garden suite (3rd unit)

- Land severance and new home build

Additionally, I will be looking to implement as many of the following to maximize upside potential while minimizing downside:

These include:

- Choosing the right city or town to invest in, with good local economic fundamentals, and a progressive approach to housing opportunities.

- Going through municipal websites to identify specific areas of public investment that will likely drive values higher for certain areas of the city compared to others (e.g. transportation or business improvement areas).

- Investing in modest entry level properties that would be more insulated from an economic downturn.

- A property that I can force appreciation to that I have direct control over (see forced value ladder above). I can’t do that with a condo or a small commercial unit.

- Looking for creative cash flow strategies (can a portion of the property be rented for other uses?)

- Adding additional legal units

- Purchasing within slower periods of the seasonal cycle when possible (i.e. winter and summer)

- Negotiating a better price by creating a win-win scenario with the seller (e.g. flexible closings, vendor take back mortgages, moving assistance if needed)

So these are all things that can help mitigate the effects of a market that may go down. And if the market continues to head in the same direction, all of these strategies are a big bonus.

The reason why I spend so much time outlining my understanding of the macro-economy is because I feel like it is the foundation for everything we are doing.

If you don’t at least try to understand it to your best ability, then everything else is a guessing game.

Many of us spend hours comparing prices online for products trying to save a few bucks, but yet don’t spend enough time looking at factors that can drive our investments one way or another in the hundreds of thousands.

You may be saying that the system is broken and it needs to be fixed, and that the government should do this or do that to fix it.

As bad as our current government is, I don’t think that things will improve much when the opposing party gets in power.

As George Carlin said,

I’ve long since given up on thoughts that the government can or should fix things. This is because as an observer of the trends and history, there’s really no point.

No single person, political party or any government really has the ability to change the big picture. These are really long term cycles that need to play out.

The only thing we can do is observe them, identify ways to protect and benefit ourselves and our families, and even make small contributions at the local level to improve things.

It’s cliche to say, but at the end of the day, “It is what it is”.

Save your valuable energy from complaining, and redirect that energy to building things, creating a better life for yourself, your family and your local community.

Basically it can be summarized like this. When it rains, you can either yell at the clouds, or bring an umbrella and enjoy the outdoors.

Best of luck, and thanks for reading!